You should consider the Fund’s investment objectives, risks, and charges and expenses carefully before you invest. The Prospectus details the Fund’s objective and policies, charges, and other matters of interest to a prospective investor. Please read the Prospectus carefully before investing. The Prospectus may be obtained by visiting the website at fpa.com, by email at [email protected], toll-free by calling 1-800-982-4372 or by contacting the Fund in writing.

Average Annual Total Returns (%)

Index data source: Morningstar.

Past performance is no guarantee, nor is it indicative, of future results. Current performance may be higher or lower than the performance shown. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment it may be worth more or less than its original cost. Current month-end performance data, which may be lower or higher than the performance data quoted, may be obtained at fpa.com or by calling toll-free, 1-800-982-4372. The Fund’s Total Annual Operating Expenses are 0.94% (Investor Class), 0.88% (Advisor Class), and 0.80% (Institutional Class).

The FPA Queens Road Small Cap Value Fund (“Fund”) commenced operations on June 13, 2002 (Inception date). Fund performance shown is for the Investor Class shares (QRSVX). Periods greater than one year are annualized. Fund performance is shown net of all fees and expenses and includes reinvestment of all distributions. Fund performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares, which would lower these figures. An investor cannot invest directly in an index.

Prior to November 1, 2020, the performance shown reflects the historical performance of the Fund when Bragg Financial Advisors, Inc. (“BFA”) served as investment adviser of the Fund.

From inception of the Fund to December 31, 2004, BFA and its affiliates voluntarily absorbed certain expenses of the Fund and voluntarily waived its management fee. Had BFA not done this, returns would have been lower during that period. Effective January 1, 2005 through October 31, 2020, BFA charged a single unitary management fee and contractually agreed to pay all operating expenses of the Fund except for brokerage, taxes, interest, litigation expenses, and other extraordinary expenses. Prior to November 1, 2020, the Fund had a unitized fee structure that limited annual operating expenses to 1.18%.

Please see additional important disclosures at the end of this Commentary.

Dear Fellow Shareholder:

The FPA Queens Road Small Cap Value Fund (“Fund”) returned 6.07% in the first quarter of 2026 vs. 4.96% for the Russell 2000 Value Index (“R2KV”). As a reminder, we expect to outperform in down markets and trail in speculative markets as a result of our diligent, disciplined, and patient process.

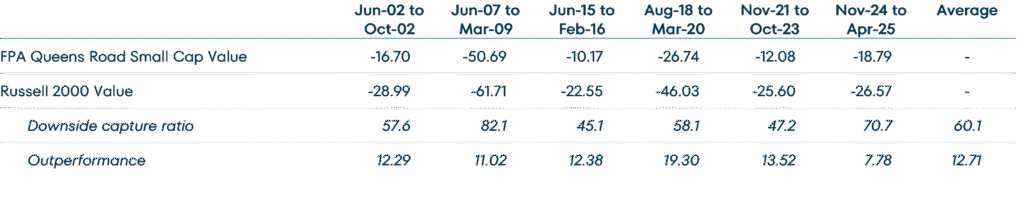

20% or Larger Russell 2000 Value Drawdowns Since Fund Inception (%)1

Market Commentary

Q1 was volatile, driven mostly by the war in Iran. We don’t have much to contribute on the current global commodity shock, political machinations, or macro-economic fallout. Instead, we try to give our readers insight into small-caps as an asset class and how we apply our long-term, fundamental investment process. From that perspective, not much has changed since last year.

In 2025, we used these letters to make three inter-related points 1) Small-caps as an asset class are relatively cheap compared to large-caps and reasonably valued from an absolute perspective. 2) There are significant differences in the quality of small public companies. In many cases, shares of quality small companies are selling at very reasonable valuations. 3) Small-caps are out of favor and we believe that the number of investors that look at small-caps through our long-term, fundamental lens has declined. We think that less competition could mean more opportunity for us. Similarly, short-term market volatility can create opportunity for those willing to look out three-to-five years. And while our rigorous and conservative research process can be slow, the number of stocks working through our “funnel” has increased.

As the Fund and strategy grow, we continue to make operational and administrative improvements that will benefit our investors over the long term. In Q1, we onboarded an additional portfolio rebalancing tool that allows us to dispose of securities through a redemption-in-kind mechanism similar to that used by ETFs. Trading in this manner allows us to exit a collection of stocks with minimal market impact. But it has the secondary benefit of potentially reducing capital gain distributions to our clients. In Q1, we eliminated a little less than $36m of capital gains.2 We think our current set of tools, coupled with our generally low-turnover approach, should support our goal of low-single digit capital gains distributions going forward. If you would like to discuss these actions in more detail, please reach out to us.

The redemption in kind trade executed this quarter, and Reflow, an additional liquidity service we started using last year, are meaningful improvements in our execution. There was a fair amount of complexity and elbow grease required to implement these tools, and, as always, we benefit from administrative support from throughout the FPA organization. We are extremely thankful for everyone’s competence and hard work. There are several other upgrades currently taking place behind the scenes that will similarly benefit investors – we will fill you in as these cross the finish line and go into production.

Portfolio Commentary

In Q1, we continued to rebalance the portfolio towards what we believe are higher quality holdings. We sold roughly 5% of the Fund’s portfolio in a single liquidity trade that took advantage of the Fund’s redemption in kind mechanism. In a volatile but positive quarter, the Fund modestly outperformed its benchmark, the Russell 2000 Value Index (“R2KV”).3

For us, the three most important elements of quality are balance sheet strength, earnings consistency, and returns on capital. Balance sheet strength helps a company overcome challenges and protects on the downside. Earnings consistency indicates that the company is likely to continue being profitable going forward. And high returns on capital suggest the company uses its resources to produce economic value.

In Q1, we added two new positions – First American Financial (FAF) and Dorman Products (DORM).

First American Financial is a title insurer that also facilitates escrow and closing services. Title insurance is relatively consolidated and, crucially, First American also owns a leading data repository of transactions called the “title plant”. Revenues are currently depressed with residential existing home sales averaging about 4m vs. a more normal rate of about 5.5m.4 FAF is currently overcapitalized, pays a ~4% dividend yield and has historically, opportunistically bought back shares.

Dorman Products manufactures and sells aftermarket car parts. The company scores well on our dashboard, having grown historically at a consistent mid-single digit rate, with high returns on capital in a non-cyclical industry. Debt to EBITDA is less than 1x, and DORM uses its cash flow to buy back stock. 2026 earnings will tick down as the company laps an accounting treatment that allowed Dorman to put lower cost, pre-tariff inventory through its cost of goods sold. Dorman is currently trading at a discount to its historical earnings multiple and we believe its shares are attractively priced

We made a significant addition to our holding in ePlus (PLUS).5 We added ePlus to the portfolio in the second half of 2025 and a discussion of the company can be found in the 25Q4 letter.

We sold our positions in Qorvo (QRVO), VSE Corp (VSEC) and Deckers (DECK). Qorvo manufactures radio frequency chips, primarily for cell phones, and is being acquired in a cash and stock deal by competitor Skyworks (SKWS).6 VSE Corp services the commercial aero aftermarket and has performed exceptionally well in a cyclically hot market. We had been trimming and the Fund’s position was small going into Q1. Deckers, owner of the UGG and Hoka shoe brands, was another long-time winner for the Fund. Similarly, we had already substantially trimmed our position in DECK before our full exit in Q1.

We substantially reduced our position in Everus Construction (ECG), an electrical contractor that has benefitted from its exposure to data center construction and has gotten quite expensive in our view.

Finally, RevGroup (REVG) was acquired by Terex (TEX) in a stock and cash deal.7 We continue to hold shares in the combined company, Terex.

At quarter end, our cash position was 10.4%.

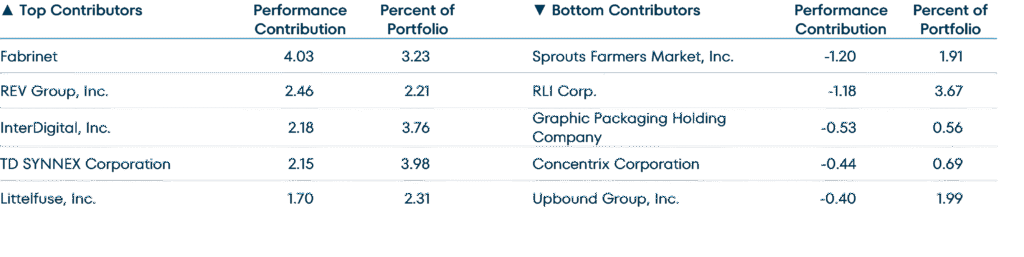

Trailing Twelve Month Top and Bottom Contributors (%)8

Top Contributors

- Fabrinet (FN) is a contract manufacturer specializing in optical networking equipment and modules. This is complex work at small scales, and Fabrinet dominates its niche. The company has experienced impressive historical revenue growth and growing operating margins. Fabrinet’s highest bandwidth products are finding increasing demand in data centers, especially those data centers used to train artificial intelligence models. In 2023, Fabrinet disclosed that Nvidia is a 10% customer. FN’s stock price has more than doubled since April of last year on rising expectations for data center spending. We believe such spending, as capitalized in FN’s stock price, may have gotten ahead of itself and have been trimming. But the need for high bandwidth networking will continue, Fabrinet dominates its core telecom and data center markets and has prudently diversified into a handful of other niches that reward precise assembly at small scale. We believe Fabrinet will be a “compounder” for many years, and we continue to hold a position.

- REV Group (REVG) is a specialty vehicle manufacturer. Most of the company’s value is in its municipal business where REV Group makes fire trucks and ambulances. The company has been reporting significant backlog and pricing growth in concert with Pierce Manufacturing (owned by Osh Kosh (OSK), another Fund holding), their primary competitor in the fire truck market. CEO Mark Skonieczny has led a significant operational restructuring, sold off the less profitable bus business, and used the proceeds to buy back stock at attractive prices. REVG’s stock price has followed improving results and performed well. On Feb 2, REV Group was purchased by Terex is a mostly stock deal.9 We continue to hold a position in the combined company, Terex.

- TD Synnex (SNX) is the largest IT distributor globally. The company has done a good job diversifying away from its historical position in hardware (PCs, peripherals, servers, networking equipment, etc.) and into software, security and services. TD Synnex is modestly levered and uses its cash flow to repurchase shares and pay dividends. The company reported blow-out earnings on Mar 31, which caused the stock price to jump.10 We think that TD Synnex is exceptionally well run, has scale and scope advantages against smaller competitors and that profits will continue to grow with IT spending at a GDP+ rate. SNX trades at roughly 11x forward earnings and continues to be a top 5 holding for the Fund.

- Littelfuse (LFUS) manufactures niche electrical components including fuses, sensors, passives and semiconductors that are sold into a broad array of end markets. Mid-single digit growth is supplemented by tuck in applications and the company has high teens operating margins and strong returns on capital. We significantly added to our position in April 2025 when the stock sold off on tariff fears. Since then, the LFUS share price has more than doubled as the company demonstrated it could navigate tariffs, sales and orders accelerated out of their post-Covid trough, and the company recorded incremental sales into data centers.

Bottom Contributors

- Sprouts Farmers Market (SFM) is a supermarket chain focusing on fresh, natural, and organic products. The company has strong operating margins, attractive returns on capital, and excellent new store economics. Through April 2025, SFM’s stock performed extremely well in concert with strong revenue growth and rising earnings estimates. As SFM’s valuation increased, we trimmed our position in late 2024 and early 2025. Then, when growth slowed in the second half of 2025, SFM’s share price collapsed. Today, SFM trades at a low-teens multiple of forward earnings and we are comfortable holding a mid-sized position.

- RLI Corp (RLI) is a specialty property and casualty insurer. The company is extremely selective in writing business. Its diversified lines include niche-y areas such as school buses, Hawaii homeowners, and surety. RLI’s unique culture, incentive structures and willingness to walk away from unprofitable business have historically led to exceptional financial performance. From 2015 through 2024, the company’s combined ratio has averaged 89.3% and its ROE has averaged 16.6% despite being weighed down by excess capital.11 We have owned RLI since 2011 and the stock usually commands a premium valuation – we were pleased to be able to add to our position at roughly 20x this year’s earnings.

- Graphic Packaging (GPK) is a vertically integrated paper packaging manufacturer with plants in the U.S. and Europe. The company is suffering from a combination of weak industry fundamentals, massive cost overruns at its new Waco, TX recycled paperboard plant, and too much debt. In October, CFO Stephen Scherger left to join Amcor and then in December, long-time CEO Mike Doss left under acrimonious circumstances.12 We are not enthused about the current situation and currently hold a less than 50 bp position in GPK.

- Concentrix (CNXC) is one of two top customer experience (CX) vendors globally. The company began by managing call centers but has since evolved into a high-tech business process outsourcer (BPO) that also designs and runs customer-facing websites and apps, integrates the data, and optimizes a client’s customer interactions. The March, 2023 acquisition of WebHelp helped consolidate the industry but left the company with roughly three turns of debt. Over the past two years, growth and margins have declined, and the market is concerned that Concentrix’s core businesses are being disrupted by AI. The company trades at very low valuation multiples, but we share the market’s concern and currently hold less than 50 bps of CNXC.

- Upbound Group (UPBD) lends to sub-prime consumers in two primary segments: Rent-a-Center, which focuses on furniture and appliances through physical stores; and Acima, which offers last-look financing through associated retailers including electronics and tire shops. Sub-prime consumers are struggling but Upbound’s operating results have hung in there. The company has been slow to de-lever after purchasing Acima in 2021 and made another incremental acquisition on Jan. 31, 2025 when it bought Brigit, an app that charges subscription fees to access payday lending. UPBD stock is cheap at less than five times earnings. But we have been slow to add given the company’s leverage and questions about its business model.

Conclusion

We are diligently focused on the long-term fundamental performance of our investments but can’t control short-term performance. We never make predictions about market direction, but we feel good about the Fund’s long-term prospects. And we will continue to manage our portfolio with diligence, discipline, and patience.

As always, and as significant co-investors in the Fund, we appreciate your trust in us to be good stewards of your capital. If you would like to discuss performance or the Fund’s portfolio holdings in greater detail, please let us know.

Respectfully,

Steve Scruggs, CFA, Portfolio Manager

Ben Mellman, Portfolio Manager

March 31, 2026

1 As of March 31, 2026. Source: Morningstar Direct, FPA. Data shown for the FPA Queens Road Small Cap Value Fund – Investor Class (“Fund”). Inception of the Fund was June 13, 2002. The periods referenced above reflect Russell 2000 Value drawdowns 20% or greater and are calculated from that index’s peak and trough dates, (i.e., 6/28/2002-10/9/2002, 6/4/2007-3/9/2009, 6/23/2015-2/11/2016, 8/22/2018-3/23/2020, 11/8/2021-10/27/2023, 11/25/2024-4/8/2025). Please see page 1 for net performance of the Fund since inception. Please also see the end of this commentary for Important Disclosures and Definitions of Key Terms.

2 Source:Mutual Fund Administration, LLC., FPA

3 FPA Queens Road Small Cap Value Fund outperformed Russell 2000 Value Index net of fees across all share classes. Average annual total returns for all share classes are available at https://fpa.com/fund/fpa-queens-road-small-cap-value-fund/

4 Source: Mortgage News Daily; https://www.mortgagenewsdaily.com/data/existing-home-sales

5 We define a significant addition as increasing our holdings by 33% or more in positions where we have a portfolio weight of at least 1% at the previous quarter end

6 Source:https://www.qorvo.com/newsroom/news/2025/skyworks-and-qorvo-to-combine-to-create-22-billion-us-based-leader

7 Source: https://investors.terex.com/news/news-details/2026/TEREX-AND-REV-GROUP-COMPLETE-MERGER-CREATING-A-PREMIER-SPECIALTY-EQUIPMENT-MANUFACTURER/default.aspx

8 Reflects the top contributors and top detractors to the Fund’s performance based on preliminary contribution to return for the trailing twelve months (TTM) period ending March 31, 2026. Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. Portfolio weights represent the average weights over the periods noted. A copy of the methodology used and a list of every holding’s contribution to the overall Fund’s performance during the quarter to date (QTD) and year to date (YTD) is available by contacting [email protected]. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities listed. Totals may not sum due to rounding. Note: December 31, 2025 company descriptions were developed by the investment team and unless otherwise noted reflect the most recent data made available by the companies or third-party research firms the investment team believe to be reliable

9 Source: https://revgroup.com/terex-and-rev-group-complete-merger-creating-a-premier-specialty-equipment-manufacturer/

10 Source: https://ir.tdsynnex.com/financials/quarterly-results/default.aspx

11 Source: RLI 10-Ks, presentations and earnings calls, FPA Queens Road Funds interpretation and adjustments; https://investors.rlicorp.com/overview/default.aspx

12 Source: https://www.packagingdive.com/news/graphic-packaging-international-ceo-ouster-reversal-eminence-capital-shareholder-board/808358/

Important Information

This Commentary is for informational and discussion purposes only and does not constitute, and should not be construed as, an offer or solicitation for the purchase or sale of any securities, products or services discussed, and neither does it provide investment advice. Any such offer or solicitation shall only be made pursuant to the Fund’s Prospectus, which supersedes the information contained herein in its entirety. This Commentary does not constitute an investment management agreement or offering circular.

The statements contained herein reflect the opinions and views of the portfolio managers as of the date written, is subject to change without notice, and may be forward-looking and/or based on current expectations, projections, and/or information currently available. Such information may not be accurate over the long-term. These views may differ from other portfolio managers and analysts of the firm as a whole and are not intended to be a forecast of future events, a guarantee of future results or investment advice.

Portfolio composition will change due to ongoing management of the Fund. References to individual securities or sectors are for informational purposes only and should not be construed as recommendations by the Fund, the portfolio manager, the Adviser, the Sub-Adviser or the distributor. It should not be assumed that future investments will be profitable or will equal the performance of the security or sector examples discussed. The portfolio holdings as of the most recent quarter-end may be obtained at fpa.com.

Future events or results may vary significantly from those expressed and are subject to change at any time in response to changing circumstances and industry developments. The information and data contained herein has been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data.

The information contained herein is not complete, may change, and is subject to, and is qualified in its entirety by, the more complete disclosures, risk factors, and other information contained in the Fund’s Prospectus and Statement of Additional Information. The information is furnished as of the date shown. No representation is made with respect to its completeness or timeliness. The information is not intended to be, nor shall it be construed as, investment advice or a recommendation of any kind.

Certain statements contained in this presentation may be forward-looking and/or based on current expectations, projections, and information currently available. Actual events or results may differ from materially those we anticipate, or the actual performance of any investments described herein may differ from those reflected or contemplated in such forward-looking statements, due to various risks and uncertainties. We cannot assure future results and disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Such statements may or may not be accurate over the long-term. Statistical data or references thereto were taken from sources which we deem to be reliable, but their accuracy cannot be guaranteed.

The reader is advised that the Fund’s investment strategy includes active management with corresponding changes in allocations from one period of time to the next. Therefore, any data with respect to investment allocations as of a given date is of limited use and may not be reflective of the portfolio manager’s more general views with respect to proper geographic, instrument and /or sector allocations. The data is presented for indicative purposes only and, as a result, may not be relied upon for any purposes whatsoever.

In making any investment decision, you must rely on your own examination of the Fund, including the risks involved in an investment. Investments mentioned herein may not be suitable for all recipients and in each case, potential investors are advised not to make any investment decision unless they have taken independent advice from an appropriately authorized advisor. An investment in any security mentioned herein does not guarantee a positive return as securities are subject to market risks, including the potential loss of principal. You should not construe the contents of this document as legal, tax, investment or other advice or recommendations.

Fund performance presented is calculated on a total return basis, which includes the reinvestment of all income, plus realized and unrealized gains/losses, if applicable. Unless otherwise indicated, performance results are presented on a net of fees basis and reflect the deduction of, among other things: management fees, brokerage commissions, operating and administrative expenses, and accrued performance fee/allocation, if applicable.

The information provided in this presentation is based upon data existing as of the date(s) of the report and has not been audited or reviewed. While we believe the information to be accurate, it is subject in all respects to adjustments that may be made after proper review and reconciliation.

Investments carry risks and investors may lose principal value. Capital markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Securities of smaller, less well-known companies involve greater risks and they can fluctuate in price more than larger company securities. You risk paying more for a security than you received from its sale.

The Fund primarily invests in equity securities (common stocks, preferred stocks and convertible securities) of small-capitalization U.S. companies, defined as those with market-capitalization, at the time of purchase, that is no greater than the largest market-capitalization of any company included in the Russell 2000 Index. Investing in small companies involves special risks including, but not limited to, the following: smaller companies typically have more risk and their company stock prices are more volatile than that of large companies; their securities may be less liquid and may be thinly traded which makes it more difficult to dispose of them at prevailing market prices; these companies may be more adversely affected by poor economic or market conditions; they may have limited product lines, limited access to financial resources, and may be dependent on a limited management group; and small-cap stocks may fluctuate independently of large-cap stocks. All investment decisions are made at the discretion of the Portfolio Manager, in accordance with the then current Prospectus. Comparison to any index is for illustrative purposes only.

The prices of securities held by the Fund may decline in response to certain events taking place around the world, including those directly involving the companies whose securities are owned by the Fund. Securities in the Fund’s portfolio may underperform due to inflation (or expectations for inflation), interest rates, global demand for particular products or resources, natural disasters, pandemics, epidemics, terrorism, regulatory events and governmental or quasi-governmental actions. There is a risk that you may lose money by investing in the Fund.

Value style investing presents the risk that the holdings or securities may never reach their full market value because the market fails to recognize what the portfolio management team considers the true business value or because the portfolio management team has misjudged those values. In addition, value style investing may fall out of favor and underperform growth or other styles of investing during given periods.

Please refer to the Fund’s Prospectus for a complete overview of the primary risks associated with the Fund.

©2026 Morningstar, Inc. All Rights Reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted by Morningstar to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The FPA Funds are distributed by Distribution Services, LLC. 190 Middle Street, Suite 301, Portland, ME 04101. Distribution Services, LLC and FPA are not affiliated.

Index Definitions

Comparison to any index or benchmark is for illustrative purposes only and should not be relied upon as a fully accurate measure of comparison. The Fund may be less diversified than the indices noted herein and may hold non-index securities or securities that are not comparable to those contained in an index. Indices will hold positions that are not within the Fund’s investment strategy. Indices are unmanaged and do not reflect any commissions, transaction costs, or fees and expenses which would be incurred by an investor purchasing the underlying securities and which would reduce the performance in an actual account. You cannot invest directly in an index.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. It is a market cap weighted index that includes the smallest 2,000 companies covered in the Russell 3000 universe of United States-based listed equities.

The Russell 2000 Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies that are considered more value oriented relative to the overall market as defined by Russell’s leading style methodology.

Standard & Poor’s 500 Stock Index (S&P 500) is a-capitalization-weighted index which covers industrial, utility, transportation and financial service companies, and represents approximately 75% of the New York Stock Exchange (NYSE) capitalization and 30% of NYSE issues. The S&P 500 is considered a measure of large-capitalization stock performance.

Standard & Poor’s 600 Stock Index (S&P 600) is an index of small-cap stocks managed by Standard & Poor’s. It tracks a broad range of small-sized companies that meet specific liquidity and stability requirements. This is determined by specific metrics such as public float, market capitalization, and financial viability, among other factors.

Small-cap Value Companies: The term small-cap describes companies with a relatively small market-capitalization. A company’s market-capitalization is the market value of its outstanding shares. The definition for small-cap varies, but generally means a company with $300 million to $2 billion in market-capitalization.

Glossary of Terms

Compounders: High quality companies the Fund hopes to own forever. The two most important quality metrics are earnings consistency and returns on invested capital. Quality means the Fund can have confidence that a business will create shareholder value over the long-term.

Downside-capture ratio is used to evaluate how well an investment manager performed relative to an index during periods when that index has fallen. The ratio is calculated by dividing the manager’s returns by the returns of the index during the down market, and multiplying that factor by 100. BPS or basis points; 1 bps is equal to 0.01%.

Earnings per share (EPS) is calculated as a company’s profit divided by the outstanding shares of its common stock.

Expected earnings are an estimate for a company’s future quarterly or annual earnings per share (EPS).

Forward earnings are an estimate of the next period’s earnings of a company, usually through the completion of the current fiscal year and sometimes to the following fiscal year.

Free Cash Flow represents the cash a company can generate after required investment to maintain or expand its asset base.

Margin of Safety – Buying with a “margin of safety” is when a security is purchased at a discount to the portfolio manager’s estimate of its intrinsic value. Buying a security with a margin of safety is designed to protect against permanent capital loss in the case of an unexpected event or analytical mistake. A purchase made with a margin of safety does not guarantee the security will not decline in price.

Market Cycle Performance is defined as a period that contains a decline of at least 20% from the previous market peak over at least a two-month period and a rebound to establish a new peak above the prior market peak.

Price/Earnings Ratio (P/E) is the price of a stock divided by its earnings per share. Percentages are based on the absolute number of shares. P/E ex-Neg EPS is Price/Earnings ex negative earnings per share. P/E, average P/E, or P/E (trailing) is based on the last 12 months of actual earnings. P/E, next 12 months or P/E (forward) utilizes forward earnings expectations over the next 12 months to calculate the ratio.

Return on Equity (ROE) measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested.