You should consider the Fund’s investment objectives, risks, and charges and expenses carefully before you invest. The Prospectus details the Fund’s objective and policies and other matters of interest to the prospective investor. Please read the Prospectus carefully before investing. The Prospectus may be obtained by visiting the website at fpa.com, by calling toll-free, 1-800-982-4372, or by contacting the Fund in writing.

Trailing Performance (%)

| As of June 30, 2025 | Since Inception* | 30 Yr | 20 Yr | 15 Yr | 10 Yr | 5 Yr | 3 Yr | 1 Yr | YTD | QTD | 3/25/00–10/9/07 | 10/10/07–1/3/22 | 1/4/22–6/30/25 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FPA Crescent (FPACX) | 10.10 | 9.87 | 8.34 | 9.47 | 8.69 | 13.71 | 15.26 | 13.32 | 8.14 | 8.36 | 14.70 | 7.65 | 8.76 |

| MSCI ACWI** | – | – | – | – | 9.99 | 13.65 | 17.35 | 16.17 | 10.05 | 11.53 | – | 6.33 | 7.48 |

| S&P 500 | 10.58 | 10.47 | 10.73 | 14.86 | 13.65 | 16.64 | 19.71 | 15.16 | 6.20 | 10.94 | 2.00 | 10.43 | 9.32 |

| 60% MSCI ACWI / 40% BBG U.S. Agg | – | – | – | – | 6.87 | 7.87 | 11.35 | 12.14 | 7.70 | 7.34 | – | 5.74 | 4.29 |

| 60% S&P 500 / 40% BBG U.S. Agg | 8.37 | 8.27 | 7.90 | 9.92 | 9.01 | 9.62 | 12.75 | 11.62 | 5.46 | 7.02 | 3.97 | 8.14 | 5.41 |

| CPI | 2.53 | 2.52 | 2.57 | 2.65 | 3.07 | 4.58 | 2.90 | 2.67 | 1.23 | 0.59 | 2.75 | 2.11 | 3.96 |

Index data source: Morningstar.

Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment it may be worth more or less than its original cost. Current month-end performance data, which may be lower or higher than the performance data quoted, may be obtained at fpa.com or by calling toll-free, 1-800-982-4372. The FPA Crescent Fund – Institutional Class (“Fund” or “FPACX”). Total expense ratio as of most recent prospectus is 1.06%, the Fund’s net expense ratio is 1.06% (including dividend and interest expense on short sales), the adjusted expense ratio is 1.05% (after reimbursement and excluding dividend and interest expense on short sales).

Calculated using Morningstar direct. Periods greater than one year are annualized. Fund performance is shown net of all fees and expenses. Fund performance is calculated on a total return basis which includes reinvestment of all distributions. Fund returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares, which would lower these figures. Comparison to any index is for illustrative purposes only. An investor cannot invest directly in an index. The Fund does not include outperformance of any index or benchmark in its investment objectives.

* The Fund commenced operations on June 2, 1993. The performance shown for periods prior to March 1, 1996 reflects the historical performance of a predecessor fund. FPA assumed control of the predecessor fund on March 1, 1996. The Fund’s objectives, policies, guidelines, and restrictions are, in all material respects, equivalent to those of the predecessor fund.

** The MSCI ACWI was not considered a relevant illustrative index prior to 2011 because the Fund was not classified as having global mandate until this point in time. Market Cycle Performance for MSCI ACWI is shown for illustrative purposes only in the most recently completed market cycle (i.e., 10/10/07–01/03/22) to illustrate how global equities performed during that period.

Market Cycle Performance is defined as a period that contains a decline of at least 20% from the previous market peak over at least a two-month period and a rebound to establish a new peak above the prior market peak. Data reflects the three most recent market cycles (peak to peak). The current cycle is ongoing and thus presented through the most recent quarter-end. Once the cycle closes, the results presented may differ materially.

First Pacific Advisors, LP (the “Adviser” or “FPA”), the Fund’s investment adviser, has contractually agreed to reimburse the Fund for operating expenses in excess of 0.05% of the average net assets of the Fund, excluding management fees, administrative service fees, short sale dividend expenses and interest expenses on cash deposits relating to short sales, brokerage fees and commissions, redemption liquidity service expenses, interest, taxes, fees and expenses of other funds in which the Fund invests, and extraordinary expenses, including litigation expenses not incurred in the Fund’s ordinary course of business, through April 30, 2026. The Adviser has also contractually agreed to reimburse the Fund for redemption liquidity service expenses in excess of 0.0044% of the average net assets of the Fund through April 30, 2026. These agreements may only be terminated earlier by the Fund’s Board of Trustees (the “Board”) or upon termination of the Advisory Agreement. Note that the management fees include both an advisory fee of 0.93% and class-specific administrative service fee of 0.07%. For additional information about the administrative service fee, please see the section in the Prospectus titled “Management of the Fund.”

All data herein is representative of the Institutional Share Class. Please see important disclosures at the end of the commentary.

Dear Shareholder:

Performance Overview

The FPA Crescent Fund – Institutional Class (“Fund” or “Crescent”) gained 8.36% in Q2 2025 and 13.32% in the trailing twelve months.

Its twelve-month return was 82.4% of the global market (i.e., MSCI AWCI, the “ACWI”), outperforming its 66.9% average net risk exposure.

Performance versus Illustrative Indices (%)1

| Q2 2025 | Trailing 12-month | |

|---|---|---|

| FPA Crescent | 8.36 | 13.32 |

| FPA Crescent – Long Equity | 13.41 | 17.26 |

| MSCI ACWI | 11.53 | 16.17 |

| S&P 500 | 10.94 | 15.16 |

| 60% MSCI ACWI / 40% Bloomberg U.S. Agg | 7.34 | 12.14 |

| 60% S&P 500 / 40% Bloomberg U.S. Agg | 7.02 | 11.62 |

Portfolio & Market Discussion

Crescent’s top five performers contributed 5.10% to its trailing twelve-month return while its bottom five detracted 1.81%.

Trailing Twelve-Month Contributors and Detractors (%) as of June 30, 20252

| Top Contributors | Performance Contribution | Percent of Portfolio | Bottom Contributors | Performance Contribution | Percent of Portfolio |

|---|---|---|---|---|---|

| Meta Platforms | 1.34 | 3.1 | Int’l Flavors & Fragrances | -0.52 | 2.2 |

| Holcim/Amrize | 1.19 | 2.9 | ICON | -0.41 | 0.6 |

| Citigroup | 1.02 | 2.7 | Glencore | -0.40 | 1.1 |

| Safran | 0.81 | 1.6 | Cannabis Swap Basket | -0.25 | 0.2 |

| Nintendo | 0.73 | 1.0 | NXP Semiconductors | -0.22 | 1.0 |

| Total (Top) | 5.10 | 11.3 | Total (Bottom) | -1.81 | 5.1 |

1 Source: FPA, Morningstar. Comparison to the indices is for illustrative purposes only. The Fund does not include outperformance of any index or benchmark in its investment objectives. An investor cannot invest directly in an index. The long equity segment of the Fund is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. Long equity holdings only includes equity securities excluding paired trades, short-sales, and preferred securities. The long equity performance information shown herein is for illustrative purposes only and may not reflect the impact of material economic or market factors. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Long equity performance does not represent the return an investor in the Fund can or should expect to receive. Fund shareholders may only invest or redeem their shares at net asset value.

2 Reflects the top five contributors and detractors to the Fund’s performance based on contribution to return for the trailing twelve months (“TTM”). Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. Percent of portfolio reflects the average position size over the period. The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. A copy of the methodology used and a list of every holding’s contribution to the overall Fund’s performance during the TTM is available by contacting FPA Client Service at [email protected]. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities listed.

Past performance is no guarantee, nor is it indicative, of future results.

We will review two companies that have impacted portfolio performance but that we have not recently discussed.³

Holcim/Amrize has performed well on the back of strong business performance and a strategic decision to separate the company’s North American operations. The North American operations have taken the name Amrize and have a US listing (NYSE: AMRZ). We are pleased to see former CEO Jan Jenisch return to lead the North American business.

International Flavors & Fragrances strengthened its balance sheet through a series of asset sales. Since the beginning of 2024, new management has consistently delivered or exceeded financial targets. Despite these positive developments, the company’s shares have re-rated lower, and the stock price has declined.

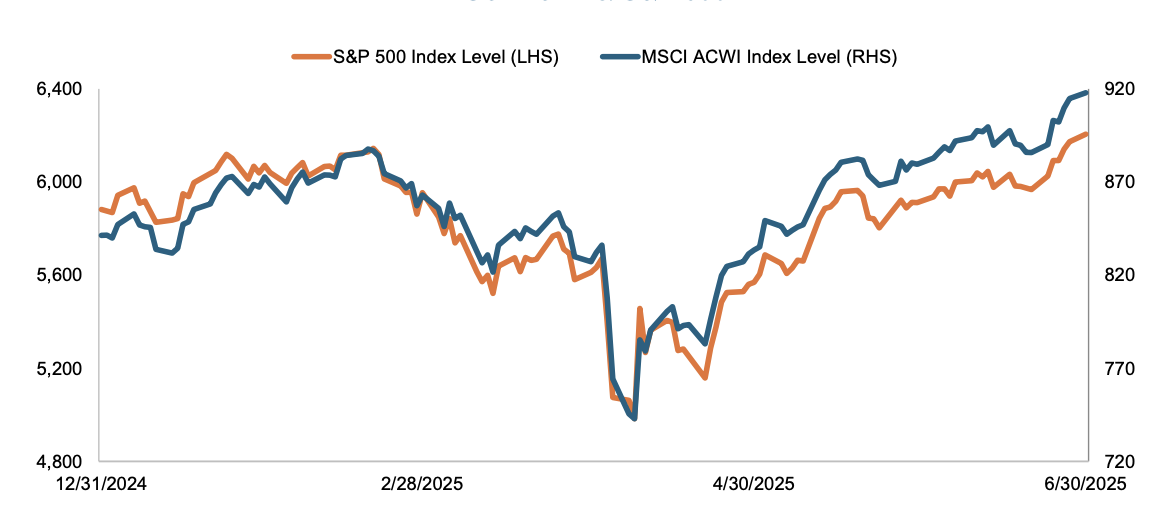

The first half of 2025 brought higher volatility, with the MSCI ACWI and S&P 500 declining by 16.3% and 18.9%, respectively, in a few days in April from their February peaks. For some people, such dramatic movement implies greater risk, but when viewed over a longer horizon, such an opinion becomes harder to defend.

Anchoring to daily pricing fluctuations can cause unnecessary stress and lead to decisions that may reduce your returns. Instead, internalizing the importance of a longer time frame should help reduce the stress caused by market volatility. We have successfully and consistently applied the discipline of looking to a longer time frame through market swings for more than thirty years.

Daily Pricing in the First Half of 2025 MSCI ACWI & S&P 5004

3 Historical commentaries for the Fund can be accessed here on the fpa.com website.

4 Source: Bloomberg. As of June 30, 2025.

Past performance is no guarantee, nor is it indicative, of future results.

Semi-Annual Pricing in the First Half of 2025 MSCI ACWI & S&P 5005

5 Source: Bloomberg. As of June 30, 2025.

Life offers little certainty, so we expect uncertainty and build models that reflect a range of potential outcomes: Low, Base, and High. We often have opportunities to acquire good businesses that have bad news and very low expectations for future performance incorporated into their stock prices. To the extent that these businesses exceed these low expectations, we expect to be rewarded. We have operated in this manner for three decades and will continue to do so. Importantly, the world is neither more nor less certain today than it was before Liberation Day. A cogent philosophy, clarity of thought, practiced execution, and repetition should enable us to navigate an ambiguous future, much like the directions you will find on shampoo bottles: “Wash, Rinse, Repeat.”

We continued to trim positions in 2024 and early 2025 in response to elevated valuations, resulting in increased cash as we await opportunities. After President Trump announced his Liberation Day tariffs on Thursday, April 2, 2025, global markets plunged, but just a few trading days later, they significantly rebounded. A stock market drawdown that lasts only a few days is too short a timeframe to materially shift the portfolio. Despite the brevity of the decline, we did selectively redeploy some capital in a few highconviction positions.

Post Liberation Day Decline and Recovery MSCI ACWI & S&P 5006

| Index | Decline April 2–8 | Recovery April 8–9 | Percent Recovery |

|---|---|---|---|

| MSCI ACWI | -11.1% | 5.7% | 51.4% |

| S&P 500 | -12.1% | 9.5% | 78.5% |

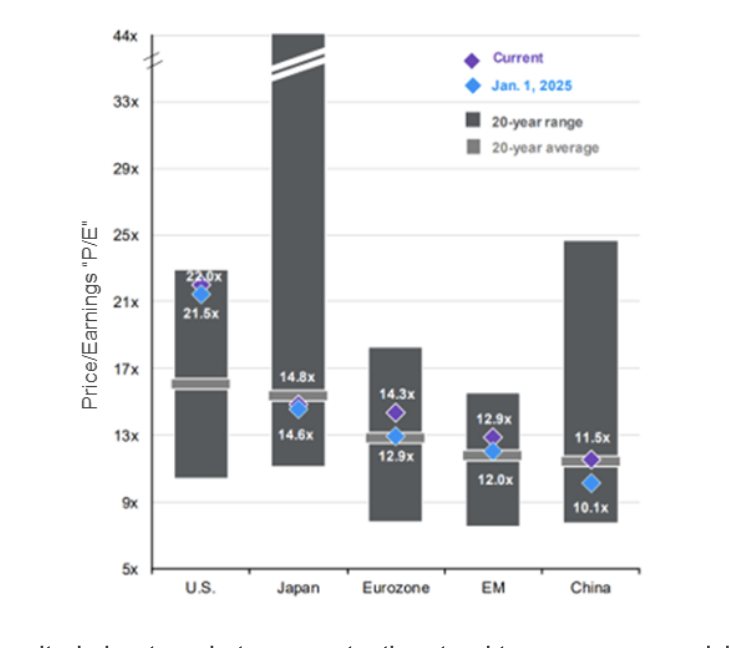

Valuations remain above average, partly justified by lower-than-average interest rates. US companies continue to trade more expensively relative to their historical average and when compared to those based outside the US, which supports our continued interest in investing overseas.

6 Source: Bloomberg.

Past performance is no guarantee, nor is it indicative, of future results.

Valuations by Country/Region P/E, next 12 months7

7 As of June 30, 2025. Source: J.P. Morgan Asset Management Guide to the Markets. Forward Price to Earnings is a version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation. The Fund does not include outperformance of any index or benchmark in its investment objectives. Please refer to the Important Disclosures for definitions of key terms and representative indices used for each geographic market shown in the table.

When people become excited about market prospects, they tend to assume more risk, which can manifest in the form of paying a higher multiple, increasing risk exposure, or sometimes using leverage (e.g., through debt or derivatives). We see that happening today. This year is the second-largest inflow year into leveraged equities as of June 10th, and the year isn’t over yet.8 Other speculative indicators help explain today’s rising stock prices. Riskier option volumes have hit new highs (e.g., 0DTE)9. Retail investors have helped lead the charge, ramping up their investments in leveraged equity funds. Retail investors are also buying more stocks on margin (FINRA margin debt has more than doubled in the last five years).10

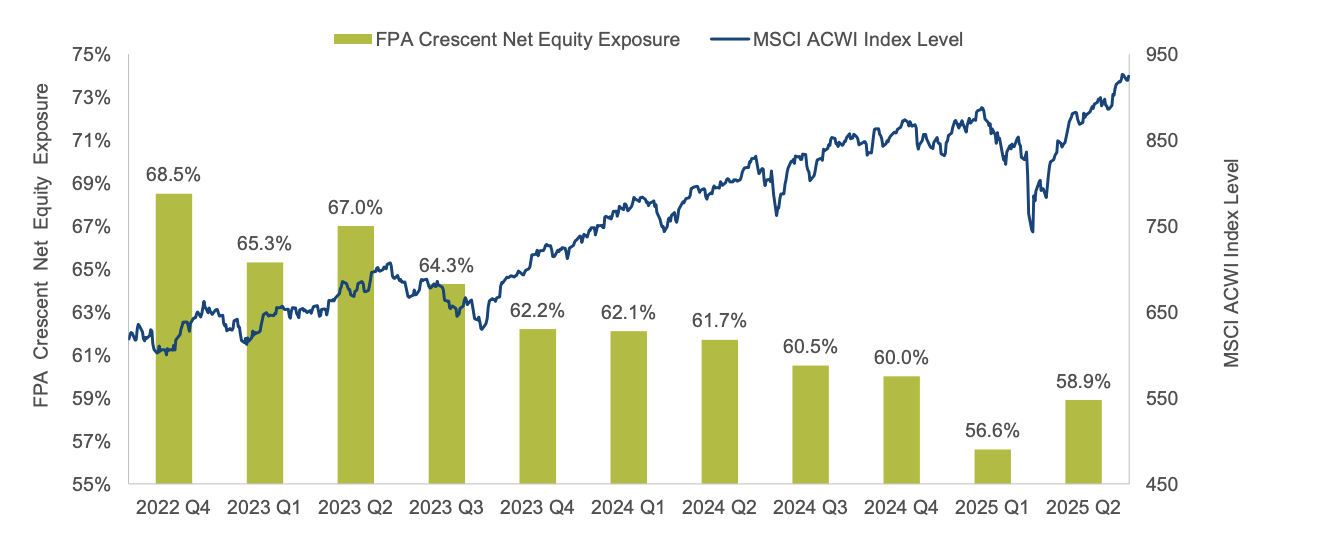

Broader risk-taking seems less appropriate given the elements of speculative excess combined with relatively high market valuations. Crescent continues to maintain a conservative posture, with risk assets ending the second quarter at 63.5%, down from 67.5% at year-end 2024 and from 69.5% a year ago. The Fund’s equity risk exposure has generally moved in inverse proportion to the market. When stock prices rise, exposure decreases, and conversely, when stock prices decline, exposure increases. This is a generalization, as sectors sometimes exhibit performances and valuations that deviate from the market as a whole. Before the recent market correction, the Fund’s net equity exposure dropped to a recent low of 56.6%. We then purchased equities during the market weakness, which caused net equity exposure to increase moderately to 58.9% at quarter-end.

8 Source: DailyShot, BofA Global Investment Strategy, EPFR. 2025 YTD as of June 10, 2025 annualized. Second largest on record.

9 Source: CBOE. As of June 30, 2025. “0DTE” stands for “zero days to expiration”.

10 Source: MacroMicro. US Margin Debt. As of June 30, 2025. “FINRA” stands for “Financial Industry Regulatory Authority”.

Past performance is no guarantee, nor is it indicative, of future results.

FPA Crescent Net Equity Exposure vs MSCI ACWI Q4 2022 vs Q2 202511

11 Source: FPA, Bloomberg. As of June 30, 2025.

Past performance is no guarantee, nor is it indicative, of future results.

As far as mutual funds go, Crescent utilizes an unusually wide range of tools and approaches to solve various problems effectively. We endeavor to avoid the cognitive bias of over-reliance on any one method. If it’s raining, for example, we’re looking for our umbrella, not our sunscreen.

Our exposure to different asset classes, regions, industries, market capitalizations, etc. shifts as a function of opportunity. For example, we believe that the intersection of risk and reward is more attractive today in small and medium-sized companies and explains the current attention we have paid to this area. Excessive attention to one area can create opportunities in another, which we believe is the case with small- to midcap (SMID) shares versus large-cap. Large-capitalization stocks, particularly those that are “growthier,” have captured the minds and wallets of investors and now trade at unusually high valuations that do not afford the downside protection we prefer should either growth be less than expected or valuation multiples contract.

Returns & Valuations by Style12

12 Source: JP Morgan Guide to the Markets 3Q25. As of June 30, 2025. https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/market-insights/guide-to-the-markets/mi-guide-to-the-markets-us.pdf

Closing

While we cannot guarantee an exact rate of return, we will continue to apply the same philosophy and process with a focus on downside protection.

Respectfully submitted,

FPA Crescent Portfolio Managers

July 25, 2025

13 Downside protection refers strictly to a strategic investment goal and is not meant to imply any guarantee against loss, including the loss of the entire principal amount invested.

Past performance is no guarantee, nor is it indicative, of future results.

FPA Crescent Fund Portfolio Highlights Footnotes

¹ Comparison to the indices is for illustrative purposes only. The Fund does not include outperformance of any index or benchmark in its investment objectives. An investor cannot invest directly in an index. The long equity performance for the Fund is presented gross of investment management fees, transactions costs, and Fund operating expenses which, if included, would reduce the returns presented. Crescent long equity excludes partial trades, short-sales, and preferred securities. The long equity performance information shown herein is for illustrative purposes only and should not be construed to represent the impact of material economic or market factors. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Long equity performance does not represent the return an investor in the Fund can or should expect to receive. Fund shareholders may only invest or redeem their shares at net asset value.

² List provides the top 10 holdings for the Fund as a percentage of total net assets.

³ Risk Assets include all investments excluding cash and cash equivalents. Net Risk Exposure is the percentage of the portfolio exposed to Risk Assets. “Other” includes derivatives, futures, limited partnerships, and US Treasuries with a maturity greater than 1 year.

⁴ Geographic exposure based on country of domicile and revenue by geography. Revenue refers to the geographic location of companies’ revenue sources, rather than where they are domiciled, and may provide insight into the portfolio’s geographic diversification. Domicile and revenue composition are shown for the FPA Crescent Fund Institutional Class’s (“Fund”) net equity positions as of June 30, 2025. Portfolio composition will change due to ongoing management of the Fund. Excludes cash and cash equivalents.

⁵ The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. The Bought/Sold table excludes positions used for cash management and positions that have not been explicitly identified in the fund’s most recent quarterly portfolio holdings report. It should not be assumed that an investment in the securities listed was or will be profitable. Increases and decreases represent securities whose position size either changed by at least 33% over the period and that represented greater than 0.75% of the portfolio at the beginning of the quarter or approximately greater than 0.25% of average NAV spent on trading. Percent of portfolio reflects the ending position size of the period. The portfolio holdings as of the most recent quarter-end may be obtained at fpa.com.

⁶ Reflects the top five contributors and detractors to the Fund’s performance based on contribution to return for the trailing twelve months (“TTM”). Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. Percent of portfolio reflects the average position size over the period. The information provided does not reflect all positions purchased, sold, or recommended by FPA during the quarter. A copy of the methodology used and a list of every holding’s contribution to the overall Fund’s performance during the TTM is available by contacting FPA Client Service at [email protected]. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities listed.

Important Disclosures

This Commentary is for informational and discussion purposes only and does not constitute, and should not be construed as, an offer or solicitation for the purchase or sale with respect to any securities, products or services discussed, and neither does it provide investment advice. Any such offer or solicitation shall only be made pursuant to the Fund’s Prospectus, which supersedes the information contained herein in its entirety. This presentation does not constitute an investment management agreement or offering circular.

Any views expressed herein and any forward-looking statements are as of the date of the publication, are those of the portfolio management team, and are subject to change without notice. Future events or results may vary significantly from those expressed and are subject to change at any time in response to changing circumstances and industry developments. This information and data have been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data.

Portfolio composition will change due to ongoing management of the Fund. References to individual securities or sectors are for informational purposes only and should not be construed as recommendations by the Fund, the portfolio managers, the Adviser, or the distributor. It should not be assumed that future investments will be profitable or will equal the performance of the security or sector examples discussed. The portfolio holdings as of the most recent quarter-end may be obtained at fpa.com.

Investments carry risks and investors may lose principal value. Capital markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. The Fund may purchase foreign securities, including American Depository Receipts (ADRs) and other depository receipts, which are subject to interest rate, currency exchange rate, economic and political risks; these risks may be heightened when investing in emerging markets. Foreign investments, especially those of companies in emerging markets, can be riskier, less liquid, harder to value, and more volatile than investments in the United States. Adverse political and economic developments or changes in the value of foreign currency can make it more difficult for the Fund to value the securities. Differences in tax and accounting standards, difficulties in obtaining information about foreign companies, restrictions on receiving investment proceeds from a foreign country, confiscatory foreign tax laws, and potential difficulties in enforcing contractual obligations, can all add to the risk and volatility of foreign investments.

Small and mid-cap stocks involve greater risks and may fluctuate in price more than larger company stocks. Short-selling involves increased risks and transaction costs. You risk paying more for a security than you received from its sale.

The return of principal in a bond investment is not guaranteed. Bonds have issuer, interest rate, inflation and credit risks. Interest rate risk is the risk that when interest rates go up, the value of fixed income securities, such as bonds, typically go down and investors may lose principal value. Credit risk is the risk of loss of principal due to the issuer’s failure to repay a loan. Generally, the lower the quality rating of a security, the greater the risk that the issuer will fail to pay interest fully and return principal in a timely manner. If an issuer defaults the security may lose some or all of its value. Lower rated bonds, callable bonds and other types of debt obligations involve greater risks. Mortgage-backed securities and asset-backed securities are subject to prepayment risk and the risk of default on the underlying mortgages or other assets. High yield securities can be volatile and subject to much higher instances of default. Derivatives may increase volatility.

The ratings agencies that provide ratings are Standard and Poor’s, Moody’s, Fitch, DBRS, Kroll, and any other nationally recognized statistical rating organization (“NRSRO”). Credit ratings range from AAA (highest) to D (lowest). Bonds rated BBB or above are considered investment grade. Credit ratings BB and below are lower-rated securities (junk bonds). High-yielding, non-investment grade bonds (junk bonds) involve higher risks than investment grade bonds. Bonds with credit ratings of CCC or below have high default risk.

Value securities, including those selected by the Fund’s portfolio managers, are subject to the risk that their intrinsic value may never be realized by the market because the market fails to recognize what the portfolio managers consider to be their true business value or because the portfolio managers have misjudged those values. In addition, value style investing may fall out of favor and underperform growth or other styles of investing during given periods.

While transactions in derivatives may reduce certain risks, they entail certain other risks. Derivatives may magnify the Fund’s gains or losses, causing it to make or lose substantially more than it invested. Derivatives have a risk of default by the counterparty to a contract. When used for hedging purposes, increases in the value of the securities the Fund holds or intends to acquire should offset any losses incurred with a derivative.

Investments in private securities and limited partnerships present risks. These investments are not registered under the federal securities laws and are generally eligible for sale only to certain eligible investors. They may be illiquid, and thus more difficult to sell, because there may be relatively few potential purchasers for such investments, and the sale of such investments may also be restricted under securities laws.

Please refer to the Fund’s Prospectus for a complete overview of the primary risks associated with the Fund.

In making any investment decision, you must rely on your own examination of the Fund, including the risks involved in an investment. Investments mentioned herein may not be suitable for all recipients and in each case, potential investors are advised not to make any investment decision unless they have taken independent advice from an appropriately authorized advisor. An investment in any security mentioned herein does not guarantee a positive return as securities are subject to market risks, including the potential loss of principal. You should not construe the contents of this document as legal, tax, investment or other advice or recommendations.

Index Definitions

Comparison to any index is for illustrative purposes only and should not be relied upon as a fully accurate measure of comparison. The Fund may be less diversified than the indices noted herein, and may hold non-index securities or securities that are not comparable to those contained in an index. Indices will hold positions that are not within the Fund’s investment strategy. Indices are unmanaged and do not reflect any commissions, transaction costs, or fees and expenses which would be incurred by an investor purchasing the underlying securities and which would reduce the performance in an actual account. You cannot invest directly in an index. The Fund does not include outperformance of any index in its investment objectives.

60% MSCI ACWI/40% Bloomberg US Aggregate Index is a hypothetical combination of unmanaged indices comprised of 60% MSCI ACWI Index and 40% Bloomberg U.S. Aggregate Bond Index.

Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics. The CPI is presented to illustrate the Fund’s purchasing power against changes in the prices of goods as opposed to a benchmark, which is used to compare the Fund’s performance. There can be no guarantee that the CPI will reflect the exact level of inflation at any given time.

MSCI ACWI NR USD Index (MSCI ACWI) is an unmanaged free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. Net Return (NR) indicates that withholding taxes are applied to dividend reinvestments. MSCI uses withholding tax rates applicable to Luxembourg holding companies.

Standard & Poor’s 500 Stock Index (S&P 500) is a capitalization-weighted index which covers industrial, utility, transportation and financial service companies, and represents approximately 75% of the New York Stock Exchange (NYSE) capitalization and 30% of NYSE issues. The S&P 500 is considered a measure of large capitalization stock performance.

MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

MSCI Emerging Markets Index captures large and mid-cap representation across emerging markets countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country. Net Return (NR) indicates that withholding taxes are applied to dividend reinvestments. MSCI uses withholding tax rates applicable to Luxembourg holding companies.

MSCI Europe Index captures large and mid-cap representation across Developed Markets (DM) countries in Europe. DM countries in Europe include Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the UK.

MSCI Japan Index is designed to measure the performance of the large and mid-cap segments of the Japanese market.

Bloomberg US Aggregate Bond Index provides a measure of the performance of the US investment grade bonds market, which includes investment grade U.S. Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities that are publicly offered for sale in the United States. The securities in the Index must have at least 1-year remaining in maturity. In addition, the securities must be denominated in US dollars and must be fixed rate, nonconvertible, and taxable.

Glossary of Terms

Earnings Per Share (EPS) is calculated as a company’s profit divided by the outstanding shares of its common stock. The resulting number serves as an indicator of a company’s profitability.

Earnings yield refers to the earnings per share for the most recent 12-month period divided by the current market price per share. The earnings yield (the inverse of the P/E ratio) shows the percentage of a company’s earnings per share.

Long Equity Performance represents the performance of stocks that the Fund owned over the given time periods and excludes the long equity portion of a pair trade, short-sales, limited partnerships, derivatives/futures, corporate bonds, mortgage-backed securities, and cash and cash equivalents.

Market Capitalization refers to the total dollar market value of a company’s outstanding shares of stock.

Market Cycles, also known as stock market cycles, is a wide term referring to trends or patterns that emerge during different markets or business environments.

Net Equity Exposure includes long equity securities minus short-sales and preferred securities.

Net Risk Exposure is a measure of the extent to which a fund’s trading book is exposed to market fluctuations. In regard to the Fund, it is the percent of the portfolio exposed to Risk Assets.

Price to Earnings is the ratio for valuing a company that measures its current share price relative to its EPS. The price-to-earnings ratio is also sometimes known as the price multiple or the earnings multiple.

Trailing Price to Earnings is a relative valuation multiple that is based on the last 12 months of actual earnings.

Forward Price to Earnings is a version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation.

Risk Assets is any asset that carries a degree of risk. Risk asset generally refers to assets that have a significant degree of price volatility, such as equities, commodities, high-yield bonds, real estate, and currencies, but does not include cash and cash equivalents.

Standard Deviation is a measure of the dispersion of a set of data from its mean.

Volatility is a statistical measure of the dispersion of returns for a given security or market index. In most cases, the higher the volatility, the riskier the security. Volatility is often measured as either the standard deviation or variance between returns from that same security or market index.

©2025 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted by Morningstar to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The FPA Funds are distributed by Distribution Services, LLC, Three Canal Plaza, Suite 100, Portland, ME 04101. Distribution Services, LLC and FPA are not affiliated.